How Blockchain is Revolutionizing Trust and Transparency

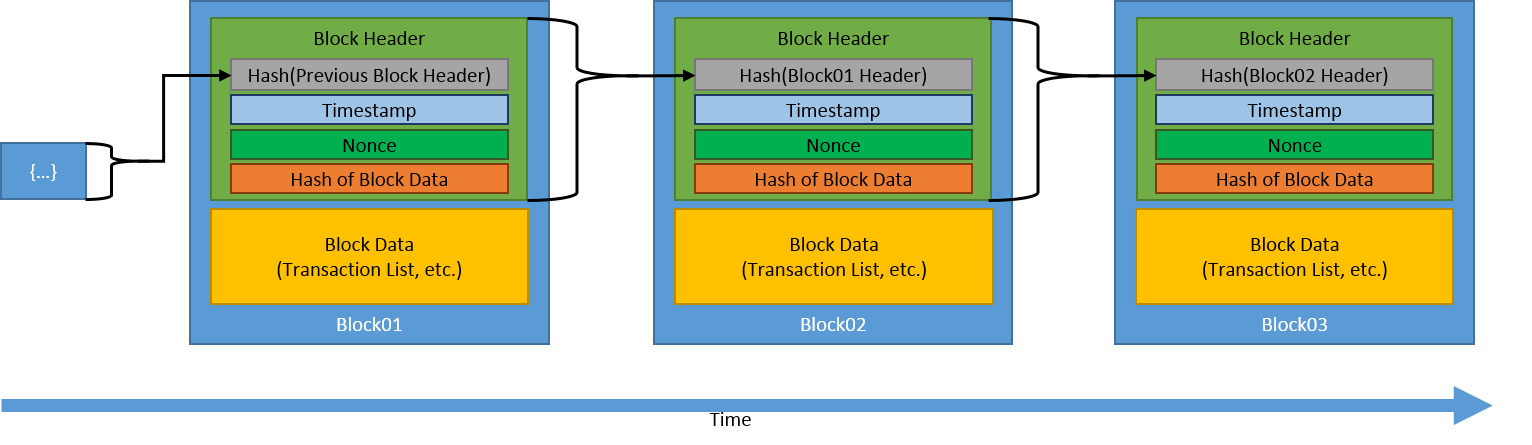

Blockchain technology is fundamentally changing the way we perceive trust and transparency in numerous sectors, including finance, supply chains, and even governance. By enabling a decentralized and immutable ledger, blockchain eliminates the need for intermediary parties, thereby reducing the chances of fraud and increasing accountability. This is particularly evident in industries like finance, where real-time transaction tracking is enhancing security and operational efficiency.

The impact of blockchain extends beyond merely enhancing financial transactions. In supply chain management, companies are leveraging this technology to provide real-time visibility into product journeys, thereby reinforcing consumer trust. A study by the IBM team illustrates how this transparency not only mitigates fraud and recalls but also empowers consumers to make informed choices about the products they purchase. By fostering greater transparency, blockchain is not only improving operational processes but also re-establishing the trust that consumers have in various systems and transactions.

Exploring the Real-World Applications of Blockchain Technology

The emergence of blockchain technology has transcended its initial association with cryptocurrencies, leading to a myriad of real-world applications across various sectors. One prominent area is supply chain management, where blockchain enhances transparency and traceability. For instance, companies like IBM have developed solutions that allow businesses to track products from origin to consumer, thereby minimizing fraud and ensuring product authenticity. In addition to supply chains, the healthcare industry is also exploring blockchain for securely sharing patient data, enabling better coordination among providers while maintaining privacy standards.

Another significant application of blockchain technology is in the realm of finance, where decentralized finance (DeFi) platforms are revolutionizing traditional banking. These platforms utilize smart contracts to facilitate peer-to-peer transactions without the need for intermediaries, thus reducing costs and increasing efficiency. Organizations like CoinDesk highlight that DeFi not only democratizes access to financial services but also empowers individuals by giving them more control over their assets. The versatility of blockchain continues to inspire innovation, from voting systems to digital identities, making it an integral part of the modern digital landscape.

What are the Key Challenges Facing Blockchain Adoption Today?

The adoption of blockchain technology is hindered by several key challenges that organizations must navigate. One major hurdle is the scalability of blockchain networks. As transaction volumes increase, many blockchains struggle to maintain speed and efficiency, leading to delays and increased costs. The limitations of current infrastructure mean that businesses seeking rapid and widespread adoption must often balance between decentralization and performance. Additionally, the lack of interoperability between different blockchain platforms poses another significant challenge, stalling progress towards a unified ecosystem.

Moreover, regulatory uncertainty remains a significant barrier to the mainstream implementation of blockchain solutions. As governments and regulatory bodies continue to grapple with the implications of decentralized technologies, the absence of clear guidelines can deter many organizations from moving forward. This uncertainty is further compounded by concerns regarding compliance with existing laws, necessitating extensive legal reviews and potential adaptations of business models. Without a robust regulatory framework, stakeholders might hesitate to invest in blockchain initiatives, stymieing its potential advantages across varying sectors.